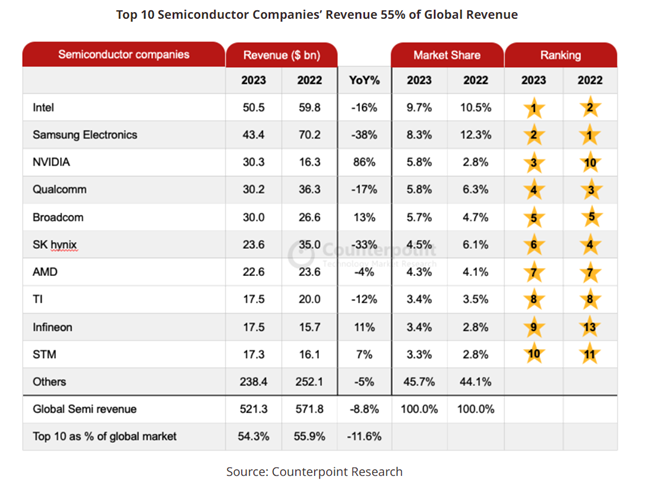

The global semiconductor industry faced an 8.8% revenue decline in 2023. This drop was primarily attributed to reduced spending in both enterprise and consumer sectors, as reported by the Counterpoint semiconductor tracker.

AI Emerges as a Key Driver in 2023

Despite challenges, AI became a key driver of content and revenue in the semiconductor industry, particularly in the second half of 2023. NVIDIA and AMD benefited the most, positioning themselves for growth in AI-related businesses in the coming years.

Counterpoint sees 2023 as a year for semiconductor companies to fine-tune strategies and manage inventory adjustments in anticipation of the upcoming AI boom.

Only 6 out of the top 20 global semiconductor vendors reported year-over-year revenue growth. The memory sector faced strong headwinds, experiencing a 43% YoY revenue decline in 2023.

Intel Leads Despite Challenges

Intel regained its top position in semiconductor revenue rankings in 2023, despite a 16% YoY revenue decline. This was largely due to a double-digit YoY shipment decline in both the PC and server segments.

Samsung reported a 38% YoY decline, heavily affected by the memory market slowdown in DRAM and NAND segments.

AI Boosts NVIDIA’s Growth

NVIDIA took the spotlight in 2023, showing an 86% YoY revenue growth and securing the third position in terms of revenue. The acceleration of AI deployments played a crucial role, with NVIDIA leading in general-purpose GPUs used in AI and high-performance computing.

Market Dynamics and Future Outlook

The top 20 global semiconductor vendors contributed to 71% of the market in 2023, down from 76% in 2022, reflecting a 14% YoY revenue decline. As the industry concludes the inventory correction cycle and client demand remains solid, supply constraints become crucial.

TSMC, the largest foundry player, maintains a positive view on capacity expansion in 2024, indicating optimism about strong demand throughout the year.

Speaking about the market dynamics, Senior Analyst William Li said:

In 2024, we anticipate artificial intelligence (AI server, AI PC, AI smartphone, etc.) to remain a significant catalyst for organic growth in the semiconductor industry. Additionally, we foresee a resurgence in the memory sector as oversupply normalizes and demand rebounds.

The automotive sector, driven by content growth, has the potential to further stimulate the market, mirroring its role as a crucial revenue driver for Infineon and STMicroelectronics in 2023.

#Global #Semiconductor #revenues #declined #Counterpoint

Comments